Understanding the Credit Scoring System: What It Is and Why It Matters

Your credit score is more than just a number — it’s a powerful tool that can open doors to financial opportunities or, if mismanaged, close them just as quickly. Whether you’re applying for a loan, renting an apartment, or even landing a job, your credit score often plays a critical role in how others assess your financial reliability. But how exactly does the credit scoring system work?

Let’s break it down.

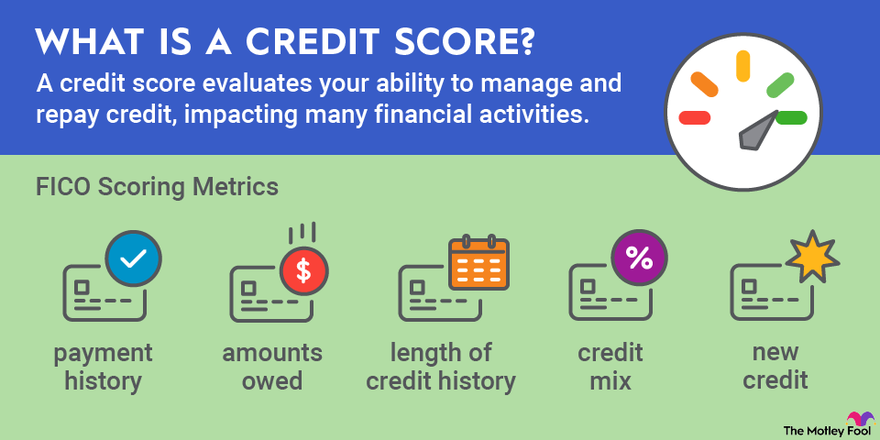

What Is a Credit Score?

A credit score is a numerical representation of your creditworthiness. It is calculated based on your credit history and indicates how likely you are to repay borrowed money. Lenders use this score to determine whether to extend credit, how much to offer, and what interest rate to apply.

Most commonly, scores range from 300 to 850, with higher scores indicating better credit health.

How Credit Scores Are Calculated

The most widely used credit scoring models, such as FICO® and VantageScore®, use similar factors when calculating your score. Here’s a basic breakdown:

- Payment History (35%)

Your record of on-time payments is the most significant factor. Missed or late payments negatively affect your score. - Credit Utilization (30%)

This refers to how much of your available credit you’re using. Ideally, keep this ratio under 30%. - Length of Credit History (15%)

The longer your credit history, the better. Lenders like to see a pattern of responsible credit use over time. - Credit Mix (10%)

A variety of credit accounts — credit cards, auto loans, mortgages — can boost your score if managed responsibly. - New Credit Inquiries (10%)

Each time you apply for credit, a hard inquiry is recorded. Too many can lower your score temporarily.

Why Your Credit Score Matters

Having a good credit score can benefit you in many ways:

- Lower interest rates on loans and credit cards

- Higher chances of approval for new credit

- Better insurance rates

- More housing and job opportunities

Conversely, a poor score can limit your options and cost you more in the long run due to higher interest rates and denied applications.

How to Improve Your Credit Score

Improving your credit score takes time and discipline, but it’s absolutely doable. Here are a few tips:

- Pay all bills on time

- Keep credit card balances low

- Don’t open unnecessary credit accounts

- Regularly check your credit report for errors

- Consider a secured credit card if you’re building or rebuilding credit

Checking Your Credit Score

You’re entitled to a free credit report from each of the three major credit bureaus — Equifax, Experian, and TransUnion — once a year via AnnualCreditReport.com. Many banks and credit card companies also provide free access to your score.

Conclusion: Take Control of Your Financial Future

Understanding how the credit scoring system works is key to taking control of your financial future. Whether you’re just starting your credit journey or looking to rebuild, knowing what affects your score and how to improve it puts you in the driver’s seat.

Start small, be consistent, and over time, you’ll see your score climb — and with it, your financial confidence.

{kind=link}